As the cost of living continues to rise, it is becoming increasingly difficult for single individuals to live comfortably. Without the safety net of a second income, the need to manage finances as a single individual is more important than ever. The process comes with unique benefits and challenges, both throughout the year and during tax time.

Budget Tips for Single Individuals

There are countless budget strategies you can use as a single individual. Some of the most popular ones are the 50/30/20 budget and the zero-based budget.

50/30/20 Budget

One of the most popular methods is the 50/30/20 budget, in which you spend about half of your after-tax income on necessities. This includes bills, groceries, housing, and all the other items that are necessary to live. Thirty percent of your income should then go to your “wants”, like dinners, entertainment, and travel. The final 20% should be designated for savings and debt repayment. These percentages can be altered to fit your own specific needs.

Zero-Based Budget

In the zero-based budget strategy, every dollar you earn is allocated to a specific expense. A certain dollar amount goes to housing, another goes to utilities, another goes to debt, and so on until every dollar in your paycheck is assigned to one expense. At the end of the pay period, whatever is left over is sent to your savings. This strategy is especially helpful in preventing impulse spending.

Retirement Tips for Single Individuals

The key to retirement savings is understanding that the earlier you start, the better. Let’s say two people begin saving $100 per month. One begins at age 25 and the other begins at age 35. The one who begins saving earlier will have nearly twice as much savings by age 65. Prioritizing any portion of your income for retirement can really maximize your savings, especially if you take advantage of employer contributions.

Automate and Maximize Your Saving

Having an emergency fund that can cover three to six months of expenses is crucial if you don’t have a second income to rely on if you lose your job or cannot work. Automating your savings can help you reach your goals faster. You can create automatic bank account transfers or even use mobile apps that schedule money transfers from your checking account to your savings account or online account. While you’re at it, you can maximize your savings by opening a high-yield savings account that will accrue interest at a higher rate than a typical savings account.

Tax Relief for Single Individuals

During tax season, it’s important to know which tax bracket you’ll fall into as a single filer. The federal income tax bracket for 2023 is as follows:

10%: $0 – $11,000

12%: $11,001 – $44,725

22%: $44,726 – $95,375

24%: $95,376 – $182,100

32%: $182,101 – $231,250

35%: $231,251 – $578,125

37%: $578,126 and up

Single filers do not qualify for deductions that many families take advantage of, so it’s also important to learn which ones you are eligible for in order to reduce your taxable income, and even your tax bracket. Remember, the tax bracket ranges above are based on taxable income, and not the actual amount of earned income you receive. In other words, the tax bracket is based on your income after deductions and credits are taken. Doing taxes on your own can be intimidating and stressful. Optima Tax Relief is the nation’s leading tax resolution firm with over $1 billion in resolved tax liabilities.

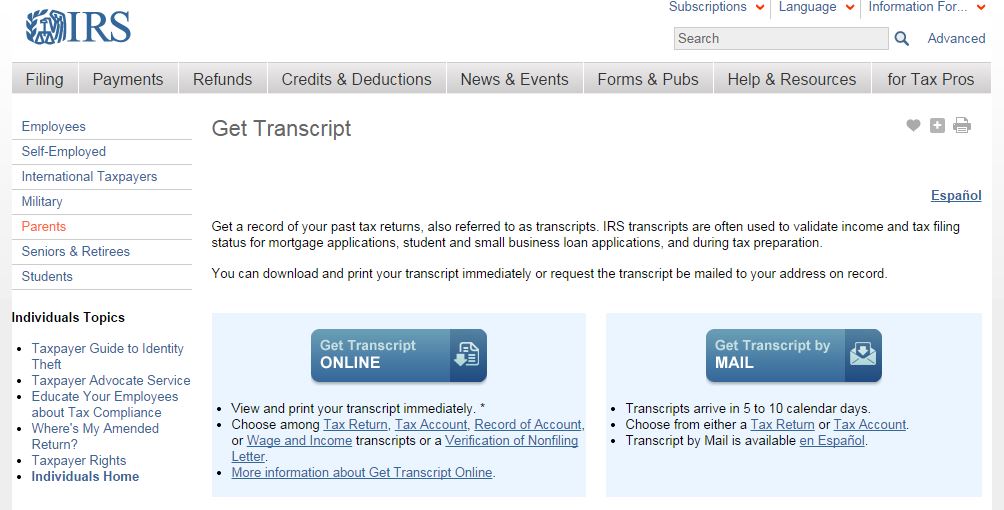

Getting a copy of your IRS transcript is easy and can be done entirely via the IRS.gov website. Follow these simple steps to retrieve your tax transcript.

Keep in mind that only transcripts for filed taxes are available. For example, if you did not file in 2003, there won’t be a tax transcript for that year. Also, if the IRS has not finished with your taxes, the transcript will not be available until they have completed those taxes.

What is an IRS Transcript used for?

IRS transcripts are typically used to validate past income and to prove income to lenders. They are often used to determine status for mortgage, student, and small business loan applications and help with tax preparation.

What information is on an IRS Transcript?

An IRS transcript includes most line items from your tax return, including all accompanying forms and schedules, as it was originally filed. Any changes made after the original filing will not be reflected. Key information listed on transcripts include marital status, AGI, taxable income, payment methods, and W-2 information.

How to get your IRS Transcript Online

You can request tax transcripts online for the current tax year and the three prior tax years. To request older transcripts, you’ll need to submit Form 4506-T. To request a transcript online:

Look under the Tools tab that is part way down the web page. Click: Get transcript for your tax records.

Once you reach the transcript page, you can request to get them by mail or continue getting them online by clicking on the box to the left, Get transcript online.

If you have gotten transcripts before, you can sign in. If not, you will need to click on the right side to create an account: Sign up.

Complete the sign up process and log in.

The next page will show a drop-down menu and ask why you need the transcript. Choose the answer that best fits your needs and continue. They ask you what you need it for so they can help you pick the right transcript.

The next page lists all your transcripts, in four different categories for all the years you filed. These include Tax Return Transcript, Record of Account Transcript, Account Transcript, and Wage and Income Transcript.

Select the transcript you need for the right year.

The site will automatically generate a PDF file of your transcript. Print it and save it.

Log out completely or close the browser when you are finished.

Make sure your pop-up blocker is off for the IRS site. It can cause errors when trying to retrieve your transcripts. If you chose mail, allow 5 to 10 business days for them to arrive before requesting another.

If you have problems navigating the website, you can contact the IRS for further assistance at 1-800-829-1040. For further assistance or help with a different tax issue, contact Optima Tax Relief. Optima Tax Relief offers a comprehensive range of tax relief services. Schedule a consultation with one of our professionals today.

The IRS is always prepared, shouldn’t you be as well? Do you need a tax relief lawyer?

Yes, absolutely.

This is a blog for a tax relief company with a small army of tax lawyers, so that’s what we’re paid to say, right? Well, yes, but it doesn’t make it any less true.

Benefits of Using a Tax Relief Lawyer: True Stories

A tax relief lawyer is a wise decision. In January, 2014, Forbes reported that Beanie Beans founder Ty Werner was convicted of evading $5.5 million dollars in taxes owed on the $27 million in interest accrued from millions of dollars stashed away in a Swiss bank account. The sentence? Two years on probation and some hefty fines, which were small change for a billionaire like Werner.

Unrelated, and a couple of months earlier, Daniel Thody, a defense contractor was found guilty to five counts of tax evasion for failing to report $15,000 and $50,000 in taxes from $1.8 million earned as a contractor for the Department of Defense. He faces up to 25 years in prison, 5 years for each count.

Which one do you think hired a tax relief lawyer and which one thought representing himself would be the smarter option? The old adage that he who represents himself has a fool for a client may be a cliché, but that doesn’t make it any less true either.

A tax attorney will ensure that you are treated better. It’s unfair, even illegal, but it’s also human nature. IRS agents are flesh and blood and if they can get away with bullying someone into their interpretation of the law, they probably will. A tax lawyer can ensure the IRS is playing by the rules and treating you fairly. IRS investigators are much more careful about asking inappropriate questions or wasting your time with unnecessary requirements if they know they are dealing with a tax attorney.

That was the finding of an investigation into nine groups in Ohio and Kentucky that sought nonprofit status. Organizations that didn’t have legal representation were more likely to have their applications stalled and receive inappropriate or unnecessary questions from the IRS.

You don’t have to worry about an IRS agent getting upset with you for hiring a tax relief lawyer either. The good ones prefer dealing with tax professionals because they don’t have to waste their time and patience explaining to you the ABCs of a tax audit or the basic IRS guidelines for a criminal investigation. In fact, hiring an experienced tax relief lawyer is generally seen as a sign of good faith to resolve your tax issues.

A few bad eggs may resent you hiring a lawyer and try to dissuade from doing so, but that’s when you really need a lawyer in your corner. The IRS’s own Declaration of Taxpayer Rights clearly states that “If you are in an interview and ask to consult such a person [a lawyer, agent or accountant], then we must stop and reschedule the interview in most cases.” Be suspicious if an IRS agent prefers not to deal with a tax professional.

Can the IRS See My Foreign Bank Account?

The IRS is a behemoth of an agency, one of the most powerful organizations on the planet. From 2008 through to 2014, over 50 bankers from Switzerland, India, Israel and other countries have been indicted for helping rich Americans squirrel billions of dollars into offshore accounts.

In 2013, the IRS also cracked the code of silence of Swiss financial institutions and got UBS, the largest Swiss Bank, to divulge confidential information on American tax evaders, and pay a $780 million penalty.

Even the IRS Thinks You Need a Tax Lawyer

The Taxpayer Advocate Service is an independent organization within the IRS which has the job of ensuring that you are treated fairly and helping you resolve problems with the IRS. Although it’s unlikely a Taxpayer Advocate Service lawyer will protect your interests quite as aggressively as a regular tax attorney, they are better than nothing, if you can’t afford to pay one.

If money is an issue, there is another option: Low Income Taxpayer Clinics. Although these clinics are partially funded by the IRS, they are completely independent and are operated by nonprofit organizations and academic institutions.

Only a Tax Attorney Can Represent You in a Criminal Investigation

Certified Public Accountants are great. When it comes to tax planning, business budgeting and asset management, a CPA is – all things being equal – more useful than a tax attorney is. But when you have a dispute with the IRS, especially if you’re accused of tax fraud or tax evasion, a tax relief lawyer is the only intelligent choice. Tax attorneys are the only ones who can represent you in a court of law and provide you the legal advice and analysis you need.

If that is not reason enough, I have two and a half words for you: attorney-client privilege. Unlike CPAs and accountants, attorneys cannot be subpoenaed to testify against a client in a criminal procedure.

Is it Worth it to Hire a Tax Attorney?

Does this mean you need a tax lawyer every time you get a letter from the IRS? No, of course not. You can probably deal with small mistakes and omissions by yourself or by giving your tax preparer a quick call. However, if there is any chance your case could go sour, you need to call a qualified and experienced tax attorney, and pronto. A good rule of thumb is that if you’re asking yourself whether it’s serious enough to merit calling a lawyer, it probably is.

A quick consultation call with a tax lawyer can save you thousands of dollars in unnecessary legal fees you could have avoided by not procrastinating. Tax lawyers know how IRS attorney think, many tax attorneys worked as IRS attorneys before hanging their own shingle. So, they know what to say, what not to say, and what buttons to push when negotiating your case.

Hiring a lawyer sends the IRS a clear and powerful message. You’re taking the investigation seriously; you’re not going to let IRS agents push you around; and you want to work with the IRS to avoid criminal charges.

The bottom line is that the IRS is scary enough when you have a first-rate lawyer at your side. So hire one already. Need to hire a tax relief lawyer? Our tax professionals at Optima Tax Relief are here to help.

Statistically, your chances of being charged with criminal tax fraud or tax evasion by the IRS are minimal. The IRS initiates criminal investigations against fewer than 2% of all American taxpayers. Of that number, only about 20% face criminal tax charges or fines.

Unofficially, the minimum amount of unpaid taxes required to trigger an IRS criminal investigation is $70,000. And since the majority of Americans don’t even earn that much money, it’s easy to see why ordinary taxpayers need never worry about facing tax evasion or tax fraud charges.

While honest mistakes or even negligence generally won’t trigger a tax investigation, perpetrating fraud very well might. IRS agents are trained to recognize signs of criminal tax fraud and evasion. Exhibiting behaviors the IRS calls “affirmative acts” could eventually result in that fateful knock on the door from the IRS.

Negligence versus Tax Fraud

Back in the day, it seemed like the IRS was lying in wait, prepared to strike unsuspecting taxpayers at the slightest sign of tax error. These days the IRS is more tolerant of mistakes made by honest taxpayers.

When the circumstances are not clear cut, the IRS frequently errs on the side of giving the taxpayer the benefit of the doubt. Miscalculating the amount of your Earned Income Tax Credit is a mistake that could cost you a significant sum of money, but it isn’t usually considered to be tax fraud. Artificially concealing $800,000 of income by keeping two sets of books? Tax fraud. (Nolo)

Evidence of Tax Fraud

Four so-called elements of tax fraud are recognized by the IRS: deception, misrepresenting material facts, submitting false or deliberately altered documents and failing to submit critical documents, such as tax returns. Several elements of fraud must occur together to trigger IRS tax fraud charges. But a single element that occurs in an especially blatant fashion may generate IRS tax fraud charges.

For instance, failure to submit a tax return for a single year is not usually considered to be an element of tax fraud. On the other hand, unless your income is extremely low, failing to file any tax returns ever could very well cause the IRS to initiate a criminal investigation against you.

Badges of Tax Fraud

The list below, taken from the IRS.gov website, represents several “badges of fraud” the IRS looks for when determining whether to file criminal charges.

Badges of tax fraud fall into four general categories: improper reporting of income, unjustified deductions or tax credits, inadequate record keeping and outright illegal behavior. As with elements of fraud, IRS agents are inclined to give taxpayers the benefit of the doubt. They’ll impose penalties for taxpayers in arrears rather than bringing criminal charges against them.

Understatement or omission of substantial sums of money

Fictitious deductions

Maintaining “shadow” sets of accounting records

Deliberate destruction of records

Evidence of consistent underreporting of income

Obviously nonsensical explanations for behavior

Refusing to cooperate with an auditor or examiner·

Deliberately concealing assets, as in overseas tax shelters

Illegal activities

Dealing exclusively in cash

Maintaining obviously inadequate records

Indicators of Fraud

The IRS categorizes indicators of tax fraud into six broad categories: income, expenses and deductions, books and records, income allocation, methods of concealment and taxpayer conduct.

Just as with elements of tax fraud and badges of tax fraud, the difference between negligence and criminal conduct is often a matter of extent.

Indicators of fraud usually include an element of deliberate conduct as well. An extensive list of actions that constitute indicators of fraud are available on the IRS website, but the examples below should provide a general idea of how the IRS views indicators of fraud.

Example #1:

Forgetting to include income from a W-2 form is not considered an indicator of income fraud. Insisting on being paid cash wages for a job and refusing to list any income from that job on your federal income tax return would be considered to be an indicator of income fraud.

Example #2:

Miscalculating the percentage of business versus personal use for your computer is not considered an indicator of fraud for expenses and deductions. Attempting to deduct the entire cost of your vacation to the Bahamas because you answered a single work-related email from your hotel room WOULD be.

Don’t Be Evasive

In general, if you suspect that a particular type of conduct is disallowed by the IRS, you shouldn’t do it. If you go ahead and do it anyway, you run the risk of being cited for tax evasion or tax fraud. And if you do receive that dreaded knock on the door from the IRS, you should not be surprised.