Disposable income serves as a key economic indicator. It reflects the financial health and spending power of individuals and households. It represents the money available after taxes, providing a glimpse into how much individuals can spend, save, or invest. However, taxes play a significant role in shaping disposable income, influencing spending patterns and economic behaviors. In this article, we break down the concept of disposable income, explore its significance, and examine how taxes impact its utilization.

What is Disposable Income?

Disposable income (DI) refers to the amount of money individuals or households have available for spending and saving after paying taxes to the government. It is the income remaining once taxes, including income tax, payroll tax, and any other deductions, have been subtracted from gross income. Essentially, it is the money that individuals can freely allocate to consumption, savings, investments, or debt repayment.

Significance

Understanding disposable income is crucial for assessing an individual’s or household’s financial well-being. It serves as a barometer for consumer spending, which is a significant driver of economic growth. Higher DI generally correlates with increased consumer spending. This in turn stimulates demand for goods and services, leading to economic expansion.

Moreover, it influences saving and investment behaviors. Individuals with higher disposable income can save more for emergencies, retirement, or large purchases. Additionally, it enables individuals to invest in assets such as stocks, bonds, real estate, or retirement accounts, fostering wealth accumulation and financial security over the long term.

Impact of Taxes on Disposable Income

Taxes have a direct impact on disposable income, as they reduce the amount of money available for consumption and saving. In addition to federal income taxes, there is also state income tax, which varies across the country with different rates, deductions, and exemptions affecting DI differently.

Income Tax

Income tax is a significant contributor to reducing DI. It is imposed on earned income, including wages, salaries, bonuses, and investment income such as interest and dividends. Progressive income tax systems levy higher tax rates on higher income levels, leading to a greater reduction in disposable income for high earners.

Payroll Taxes

Payroll taxes, which fund social insurance programs such as Social Security and Medicare, also diminish disposable income. These taxes are typically withheld from employees’ paychecks by employers. Payroll taxes are comprised of a fixed percentage of wages up to a certain limit. While payroll taxes are regressive, meaning they impose a higher burden on low-income earners, they still impact DI for all workers.

Consumption Taxes

Consumption taxes, such as sales tax or value-added tax (VAT), are levied on goods and services at the point of purchase. Unlike income taxes, which are based on earnings, consumption taxes affect spending directly, reducing disposable income with each transaction. The regressive nature of consumption taxes means that they can disproportionately impact low-income individuals, who may spend a higher proportion of their income on taxable goods and services.

Use in Taxes in Disposable Income

While taxes reduce DI, how individuals allocate their remaining funds can have tax implications as well. Several strategies can help minimize tax liabilities.

Retirement Contributions

Contributing to retirement accounts such as 401(k) plans or individual retirement accounts (IRAs) can reduce taxable income while simultaneously saving for the future. Contributions to these accounts are often tax-deductible, lowering current tax obligations and potentially increasing disposable income.

Tax-Advantaged Investments

Investing in assets with favorable tax treatment, such as municipal bonds or certain retirement accounts, can shield investment income from taxes or defer tax liabilities. This helps preserve more DI for the present.

Tax Credits and Deductions

Taking advantage of available tax credits and deductions can reduce overall tax liabilities, effectively increasing disposable income. Common tax credits include the Earned Income Tax Credit (EITC) and the Child Tax Credit, while deductions such as mortgage interest or charitable contributions can lower taxable income.

Tax Help in 2024

DI serves as a vital metric for assessing financial well-being and economic vitality. Taxes play a crucial role in shaping DI, influencing spending, saving, and investment decisions. Understanding the impact of taxes can empower individuals to make informed financial choices, optimizing their resources and maximizing their financial freedom. By employing tax-efficient strategies and leveraging available resources, individuals can effectively manage their disposable income, enhancing their economic security and prosperity. Optima Tax Relief is the nation’s leading tax resolution firm with over a decade of experience helping taxpayers with tough tax situations.

Inheriting assets can be a bittersweet experience. While it often signifies the passing of a loved one, it can also provide financial stability and opportunities for the future. However, along with the emotional and financial aspects of inheritance come tax implications, especially regarding inherited accounts. Understanding how taxes apply to inherited accounts is crucial for effective estate planning and financial management. In this article, we’ll explore the complexities of taxes on inherited accounts and explore strategies to navigate them.

SECURE Act

It’s important to know that taxes on inherited accounts is an extremely complex topic. This topic was made even more confusing by the 2019 SECURE Act and 2022’s SECURE Act 2.0. To put it simply, the SECURE Act focuses on a few key areas to improve retirement plans.

Expanded Access: Requires employers to allow long-term part-time employees who work at least 500 hours per year for three consecutive years to participate in their employer’s 401(k) plan.

Increased RMD Age: The age at which individuals must start taking required minimum distributions (RMDs) from their retirement accounts was raised from 70½ to 72. It was raised to 73 in 2023. This change allows individuals to keep their retirement funds invested for a longer period, potentially increasing their savings.

Birth or Adoption Expenses: Allows penalty-free withdrawals of up to $5,000 from retirement accounts for expenses related to the birth or adoption of a child. While the withdrawal is penalty-free, income tax still applies to the distribution.

Elimination of “Stretch” IRAs: Eliminates the “stretch” IRA provision for most non-spouse beneficiaries. Previously, non-spouse beneficiaries could stretch distributions from inherited IRAs over their lifetimes, allowing for potentially significant tax-deferred growth. Now, most non-spouse beneficiaries are required to withdraw the entire inherited IRA balance within 10 years of the original account holder’s death, potentially accelerating tax liabilities.

Knowing these provisions is key to understanding taxes on inherited accounts. The way a surviving spouse is taxed is different from the way a child or relative is taxed. Similarly, non-relatives are taxed differently. Knowing what your options are if you inherit an account can save you time, money, and a headache.

Types of Inherited Accounts

Keeping the SECURE Act in mind, we can now look at the different types of inherited accounts. Inherited accounts come in various forms, including retirement accounts like Individual Retirement Accounts (IRAs), employer-sponsored retirement plans such as 401(k)s, taxable investment accounts, and other financial assets. Each type of account may have different tax implications for beneficiaries. In most scenarios, you may inherit IRAs, employee-sponsored retirement plans, and investment accounts.

Traditional and Roth IRAs

Perhaps the most important factor that determines options when inheriting accounts is your relationship to the deceased. When inheriting a traditional IRA, beneficiaries typically must pay income tax on distributions they receive. The tax is based on the beneficiary’s individual tax rate. However, if the deceased had already begun taking required minimum distributions (RMDs), the beneficiary may need to continue taking them based on their life expectancy.

In contrast, inheriting a Roth IRA usually offers tax advantages. Qualified distributions from a Roth IRA are tax-free, so beneficiaries can potentially enjoy tax-free growth on inherited assets. However, non-qualified distributions may be subject to taxes and penalties. For example, if the Roth account is less than 5 years old at the time of withdrawal, the withdrawal may be subject to income tax.

Non-Spouse Beneficiaries

If you inherited an account from a parent, relative, or anything other than a spouse, your options are more limited. For example, you cannot roll inherited IRA funds into an IRA in your name. Also, if you plan to take RMDs using the life expectancy method, you must meet one of the following requirements:

You inherited the funds from someone who died in 2019 or earlier

You are chronically ill or disabled

You are more than 10 years younger than the deceased account owner

You are a minor child of the deceased account owner. If this is the case, you must use the life expectancy method until you reach age 18.

If you don’t meet any of these criteria, you can spread the withdrawals over a 10-year period. Alternatively, you can withdraw over 5 years or take a lump sum withdrawal.

Employer-Sponsored Retirement Plans

Similar to traditional IRAs, beneficiaries of employer-sponsored retirement plans like 401(k)s may need to pay income tax on distributions they receive. You could take a lump sum distribution, but it will be taxed as ordinary income. You could also roll the funds into your own 401(k) or IRA. If you do this, you’ll follow the same withdrawal rules. For instance, you be penalized for early withdrawals, and you must start taking RMDs by age 73. If you choose to transfer the funds into an inherited IRA account, you can make early withdrawals. On the other hand, you don’t need to move the funds at all. You can leave it in the account and take RMDs when required. However, if you are over 59½ and your spouse began taking RMDs before they passed, you can continue those withdrawals or delay it until you reach age 73 without any penalty.

Non-Spouse Beneficiaries

Once again, non-spouse beneficiaries have less options than spouses. You have three options for this type of account.

Transfer funds into an inherited IRA: This option requires the funds to be completely withdrawn within 10 years. If the money was pre-tax, you’ll pay tax on the withdrawals. If you convert a pre-tax 401(k) into a Roth IRA, you’ll likely owe taxes at the time of conversion. Withdrawing from a Roth 401(k) or converting the account to a Roth IRA has no tax implications.

Take a lump sum payment: This option generally results in a large tax bill. If you inherit a pre-tax 401(k), you’ll pay at your ordinary tax rate. If it’s a Roth 401(k), there are no tax implications.

Leave the funds and withdraw over 10 years: You can leave the funds in the original account, but you still need to meet the 401(k) 10-year rule.

Inherited Stock

Inheriting taxable investment accounts generally involves capital gains taxes. When beneficiaries sell inherited assets, they may incur capital gains tax based on the difference between the asset’s value at the time of inheritance and its value at the time of sale. However, inheriting assets also offers a “step-up” in basis, which can reduce capital gains taxes by resetting the cost basis to the asset’s value at the time of the original owner’s death.

Here’s an example. Let’s assume you sell inherited stocks one year after inheriting them. The stocks were worth $100,000 when you inherited them, and you sold them for $120,000.

Capital Gain = Sale Price – Fair Market Value at Inheritance

Capital Gain = $120,000 – $100,000 = $20,000

If your capital gains rate is 15%, you’d owe $3,000 in capital gains tax.

Capital Gains Tax = Capital Gain × Capital Gains Tax Rate

Capital Gains Tax = $20,000 × 0.15 = $3,000

Tax Help for Those Who Inherited Accounts

Inheriting accounts comes with both financial opportunities and tax obligations. Understanding the tax implications of inherited assets is crucial for maximizing their value and minimizing tax liabilities. By implementing strategic tax planning strategies and seeking professional guidance, beneficiaries can navigate the complexities of taxes on inherited accounts effectively. Optima Tax Relief has a team of dedicated and experienced tax professionals with proven track records of success.

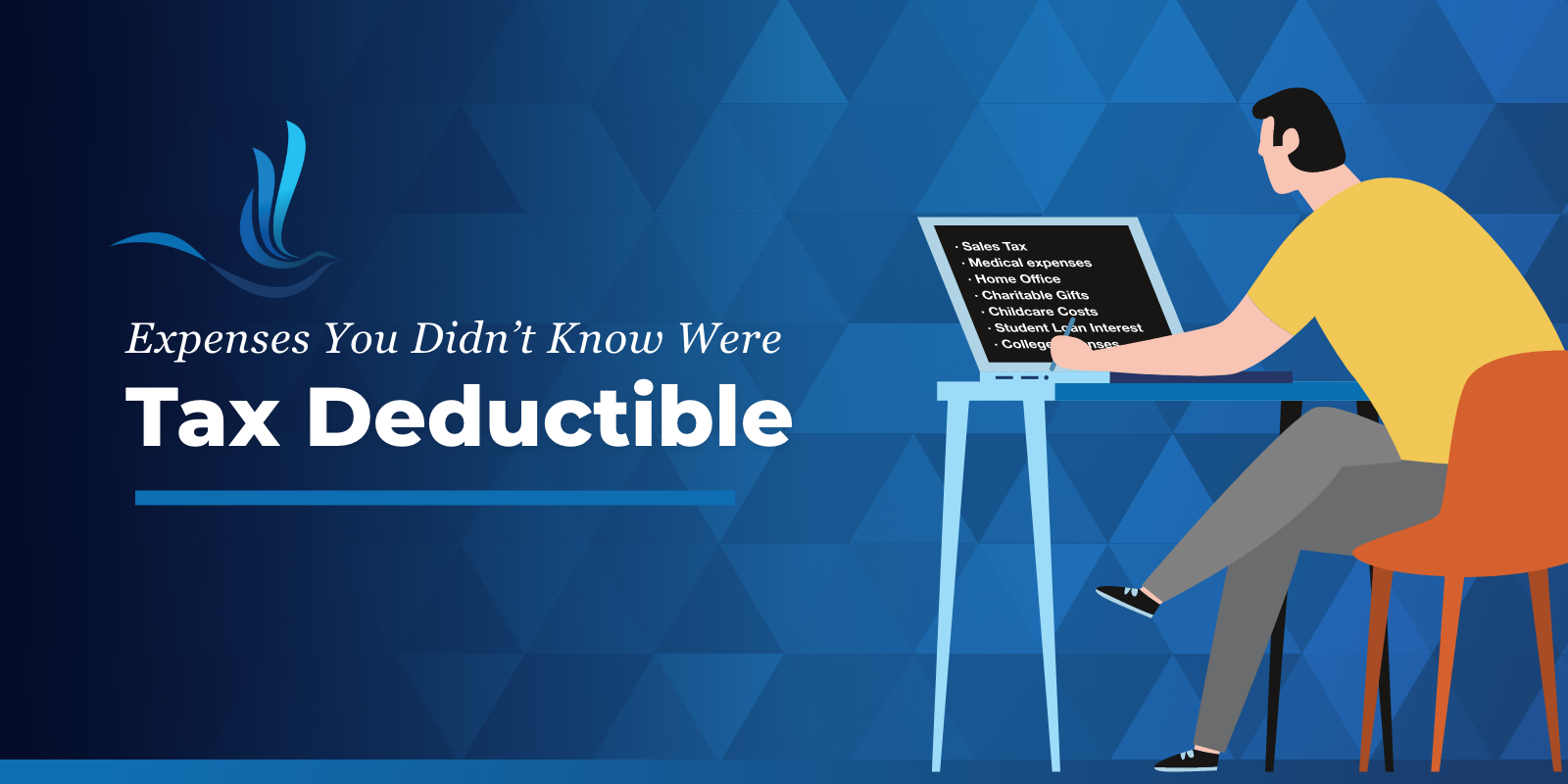

Tax deductions can help lower your tax bill and even increase your tax refund on your return. While most people are aware of common deductions like mortgage interest, charitable donations, and medical expenses, there are a plethora of lesser-known expenses that could potentially save you money on your taxes. There are several tax deductions you might not know are deductible.

Sales Taxes

For taxpayers who itemize deductions, you can deduct either state and local income taxes or state and local sales taxes paid throughout the year. In some tax years and states, it might make sense to itemize your deductions rather than take the standard deduction. This deduction can be particularly advantageous for residents of states with no income tax or for those who made significant purchases subject to sales tax. For example, if you made a large purchase like a vehicle or engagement ring, you could deduct sales taxes off your federal return. Or, if you live in a state that does not impose a state income tax, you could write off the sales tax you paid that year.

Medical Expenses

You can deduct medical expenses that exceed 7.5% of your AGI if you itemize your deductions. On the other hand, if you’re self-employed, you may be able to deduct 100% of your health insurance premiums. To qualify, you must have no other health insurance coverage. You may only deduct the amount of business income earned that year.

Home Office Deduction

Any space in your home used exclusively for conducting business can be deducted at $5 per square foot, up to 300 square feet. This home office deduction is meant for self-employed individuals. In other words, if you are a W-2 employee who works remotely, you do not qualify.

Charitable Contributions

Cash donations to approved charities can be deducted for up to 50% of your AGI. However, you must be substantiated with bank statements or receipts. Non-cash donations can be deducted at fair market value. Even out-of-pocket expenses for charitable work can be deducted. For example, you can deduct the cost of gasoline to travel to complete charitable work. Alternatively, you can deduct mileage. The standard mileage rate for charitable travel in 2023 was 14 cents per mile and it will remain at this rate in 2024.

Be sure to confirm that the charity has a tax-exempt status with the IRS before donating if you plan to claim a deduction. A few examples of approved organizations include a trust, foundation, church, synagogue, or other religious organizations, and veterans’ organizations.

Child & Dependent Care

If you pay a babysitter to watch your children while you work, look for work or attend school full-time, you may be able to claim the Child and Dependent Care Credit. This can also apply to care for an elderly parent. They must live with you and qualify as a dependent.

Student Loan Interest

If you are required to repay student loan debt, you can deduct the interest paid, up to $2,500. If your parents paid your student loan debt, the IRS views that money as a gift to you used to pay the loan. In this case, you can deduct up to $2,500 of the student loan interest they paid. That is as long as they do not claim you as a dependent on their tax return.

College Expenses

While most people are familiar with the deduction for tuition and fees, other educational expenses may also be deductible. This includes costs for workshops, seminars, and even certain textbooks and supplies. In addition, some states even allow you to deduct contributions made to your 529 College Savings Plan.

State Tax Deductions

Your state may also offer its own set of unusual tax breaks. For example, Hawaii offers a tax deduction to taxpayers who maintain an “Exceptional Tree,” like the native Norfolk Pine. This deduction is up to $3,000 per tree and can be claimed once every three years. Alaska offers a deduction of up to $10,000 to offset the cost of whaling, which involves hunting whales to give the blubber and skin back to the community. New Mexico allows its residents to stop paying state income taxes once they reach 100 years old, as long as they’ve been a resident for the last six months.

Tax Relief for Taxpayers

Every tax situation is different. There are countless deductions and credits taxpayers can claim on their federal or state returns. Overall, the best thing to do is speak with a tax preparer about which deductions and credits you are eligible for and what substantiation might be needed to claim them. However, do remember claiming deductions without proper substantiation can lead to audits and delays in processing your return.

Discovering that you owe back taxes to the IRS can be a stressful and overwhelming experience. Whether due to oversight, financial hardship, or other circumstances, it’s essential to address this issue promptly and accurately. However, determining the exact amount of back taxes owed can be complex. In this article, we’ll outline steps and resources to help you navigate the process of finding out how much you owe the IRS in back taxes.

View Your IRS Online Account

The IRS offers taxpayers access to their own IRS online account where they can view information related to their tax obligations. One of the key things you can access here is your tax balance. If you haven’t already done so, you can visit the IRS website and create an account. You’ll need to provide personal information to verify your identity and create login credentials. While the actual process of creating an IRS online account might seem tedious, the IRS takes extra precautions to safeguard your identity.

Upon logging in, you’ll see the total amount owed and balance details. Here, you should be able to see the total amount you owe the IRS, including any penalties and interest that may have accrued. Your balance is broken down by tax year for added convenience. Depending on your tax situation and the amount owed, the IRS online account portal may also provide information about payment options. This could include setting up a payment plan, making a one-time payment, or exploring other payment arrangements.

Call the IRS

The IRS has dedicated phone lines and representatives available to assist taxpayers with inquiries about their tax accounts, including outstanding tax liabilities. Before calling the IRS, gather any relevant documents, such as tax returns, notices, or correspondence from the IRS. Having this information on hand will help the representative accurately assess your tax situation. If you’re calling on behalf of someone else, you’ll need authorization to discuss their account plus their personal information.

IRS phone wait times can be long, especially during tax time. It’s recommended to contact the IRS via your online account if possible. The IRS can be reached via telephone Monday through Friday from 7am to 7pm local time. Residents of Alaska and Hawaii should follow Pacific time. Residents of Puerto Rico may call from 8am to 8pm local time. Here are the phone numbers:

Individuals: 800-829-1040

Businesses: 800-829-4933

There are also a few phone lines with their own specific hours.

Non-Profits: 877-829-5500 from 8am to 5pm local time

Estates and Gift Taxes: 866-699-4083 from 10am to 2pm Eastern time

Excise Taxes: 866-699-4096 from 8am to 6pm Eastern time

Hearing Impaired: TTY/TDD 800-829-4059

Tax Help for Those Who Owe

Once you’ve determined the amount of back taxes owed, it’s crucial to develop a plan to address your tax debt and prevent further penalties and interest accrual. Depending on your financial situation, you may consider setting up an installment agreement, making an offer in compromise, or exploring other options available through the IRS. For individuals with complex tax situations or those who need assistance navigating the process of resolving back taxes, hiring a tax professional may be beneficial. Tax professionals, such as enrolled agents or tax attorneys, can provide personalized guidance, negotiate with the IRS on your behalf, and help develop a plan to address your tax debt effectively. Optima Tax Relief is the nation’s leading tax resolution firm with over $1 billion in resolved tax liabilities.

Receiving correspondence from the IRS can be an intimidating experience for many taxpayers. Notices like CP75 or CP75A often raise concerns and questions about one’s tax situation. However, understanding what these notices entail and how to respond to them can alleviate anxiety and ensure a smoother resolution. In this guide, we’ll explore what Notice CP75 and CP75A mean, why they are issued, and steps you can take if you receive one.

Understanding Notice CP75 and CP75A

Notice CP75 and CP75A are both sent by the IRS to request verification items from taxpayers who have claimed a certain tax credit, dependents, or filing status. It will often involve the Earned Income Credit (EIC), the Additional Child Tax Credit (ACTC), and/or the Premium Tax Credit. These credits are refundable tax credits designed to assist low to moderate-income families. However, the IRS may need additional information to verify eligibility for these credits.

A CP75A Notice is similar to CP75 but is specifically for taxpayers who claimed a credit, dependent, or filing status for the first time on their tax return. Like CP75, it requests additional information to verify eligibility for these credits.

Reasons for Issuance

There are several reasons why the IRS might issue Notice CP75 or CP75A:

Incomplete Information: Your tax return may lack sufficient information or contain discrepancies that need clarification.

Verification of Eligibility: The IRS may need to verify your eligibility for the EIC and/or ACTC, especially if it’s the first time you’re claiming these credits.

Prevent Fraud: These notices help the IRS prevent fraudulent claims for refundable tax credits.

What to Do If You Receive Notice CP75 or CP75A

Receiving IRS Notice CP75 or CP75A doesn’t necessarily mean there’s a problem with your tax return. However, it’s essential to respond promptly and provide the requested information to avoid delays in processing your return and potential issues with your refund. Here’s what you should do:

Read the Notice Carefully

Take the time to carefully read through the notice to understand why it was sent and what information the IRS is requesting from you.

Gather Documentation

Collect the documentation requested in the notice, such as proof of income, residency, and dependent eligibility. Ensure that the documents are accurate and up-to-date. Depending on the credit, the notice may also be grouped with a form to fill out. Here are a few examples:

To qualify for the EIC, you’ll likely need to send back an enclosed Form 886-H-EIC.

To qualify for the Premium Tax Credit, you’ll need to send back an enclosed Form 14950.

To claim a dependent, you’ll need to submit Form 886-H-DEP.

To confirm your eligibility for a certain filing status, refer to IRS Form 14824.

Respond Promptly

The notice will provide a deadline for responding, typically 30 days. It’s crucial to adhere to this deadline to prevent further delays or complications. If you don’t respond, the IRS will likely assume you don’t want to claim the credit and then adjust your tax return accordingly.

Follow Instructions

Follow the instructions provided in the notice for submitting the requested documentation. This may involve mailing the documents to a specific address or uploading them through the IRS’s online portal.

Seek Assistance if Needed

If you’re unsure about how to respond to the notice or need assistance gathering the required documentation, don’t hesitate to seek help. You can contact the IRS directly or consult a tax professional for guidance.

Keep Records

Make copies of all documents you submit to the IRS and keep them for your records. This will help you track your communication with the IRS and provide proof of compliance if needed.

Monitor Your Mail and Online Account

Keep an eye on your mail and online IRS account for any updates or further communication regarding your case. The IRS will typically respond in 30 days with further details or next steps.

Did you Receive IRS Notice CP75 or CP75A? Call Optima

Receiving IRS Notice CP75 or CP75A can be unsettling, but it’s essential to address it promptly and provide the requested information to ensure a smooth resolution. By understanding what these notices mean and following the steps outlined in this guide, you can effectively respond to the IRS’s inquiries and safeguard your tax refund and financial interests. Remember, assistance is available if you need it, so don’t hesitate to reach out for help if you’re unsure about how to proceed. Optima Tax Relief has a team of dedicated and experienced tax professionals with proven track records of success.

In the complex world of taxes and financial regulations, backup withholding is a concept that often raises questions for taxpayers. While it might sound intimidating, it serves a crucial purpose in ensuring tax compliance and preventing underreporting of income. Let’s delve into what backup withholding entails, why it’s implemented, and how it can impact individuals and businesses.

What is Backup Withholding?

Backup withholding is a precautionary measure enforced by the IRS to guarantee that income tax is collected on certain payments. It serves as a safeguard against underreporting of income by taxpayers. It’s commonly used for those who fail to provide accurate taxpayer identification numbers (TINs) or those who have been flagged for potential underreporting or non-compliance. Backup withholding requires payers, such as employers or financial institutions, to withhold a specified percentage of certain payments to individuals. These payments typically include interest, dividends, and other types of income.

Who is Subject to Backup Withholding?

Several scenarios may trigger backup withholding:

Incorrect TIN: A taxpayer fails to provide their correct TIN to a payer. This often occurs when individuals provide incorrect Social Security numbers or employer identification numbers on tax documents.

Underreporting or Non-compliance: An individual or entity has previously underreported income, failed to file tax returns, or been subject to penalties for non-compliance. This helps ensure that taxes are collected on the correct amount of income.

Interest and Dividend Payments: Backup withholding may apply to certain types of income, including interest, dividends, and other investment earnings. It also applies to rents, royalties, gambling winnings, and other sources of income.

Failure to Certify Exemption: Certain individuals or entities may be exempt from backup withholding if they meet specific criteria outlined by the IRS. If a taxpayer fails to certify their exemption status when required, withholding may be enforced.

Exemptions

Most U.S. citizens are exempt from backup withholding if they provide their TIN or SSN with financial institutions. Certain types of income are also exempt. Common examples include:

Cancelled debts

Unemployment

State or local tax refunds

Qualified tuition program income

Real estate transactions

Retirement distributions

Employee stock ownership distributions

How Does Backup Withholding Work?

When a payer is required to initiate backup withholding, they are mandated to withhold a specified percentage of the payment before issuing it to the payee. The current backup withholding rate is typically 24% of the payment. This withheld amount is then remitted to the IRS on behalf of the payee. The withholding won’t be a surprise though. The tax filer will be notified several times of the intent to withhold.

How to Avoid

To prevent this withholding, taxpayers should ensure that their TINs are accurately provided to payers on relevant tax documents. This includes completing Form W-9 truthfully and promptly when requested by a payer. Additionally, maintaining compliance with tax filing obligations and promptly addressing any issues with the IRS can help mitigate the risk of backup withholding.

Credit for Backup Withholding

While you cannot claim a tax credit for backup withholding, the amount withheld is still considered tax already paid to the IRS. So, when you file your tax return, you will report the income subject to backup withholding, and the amount withheld will be reflected on your return. This helps ensure that you receive credit for the taxes already paid when calculating your final tax liability for the year.

Example

Let’s say you failed to report $500 in taxable income on last year’s tax return. The IRS then attempted to contact you for months letting you know you are subject to backup withholding. After six months, you open a new brokerage account and submit a W-9. On the W-9, you’ll need to cross out line item 2, which is an acknowledgment that you’re subject to this withholding. The brokerage company will then withhold 24% of your payments. At the end of the year, the brokerage company will send you a 1099 and indicate how much federal income tax was withheld on line 4. Your federal income tax liability will decrease. Furthermore, if you owe less than the withholding amount, you may receive a tax refund.

Tax Help for Those Subject to Backup Withholding

Backup withholding is a mechanism employed by the IRS to promote tax compliance. While it may seem burdensome, it serves a vital role in maintaining the integrity of the tax system. By understanding the circumstances under which backup withholding applies and taking proactive steps to comply with tax regulations, individuals and businesses can navigate the complexities of taxation more effectively. Optima Tax Relief is the nation’s leading tax resolution firm with over $1 billion in resolved tax liabilities.